CURRENT ACCOUNT

A current account is a non-interest-bearing bank account designed for businesses, firms, and professionals to facilitate high-volume, daily transactions. unlimited withdrawals, large deposits & payments.

Key Features and Benefits:

High Transaction Volume: Ideal for frequent deposits, withdrawals, and payments.

No Interest: Generally, current accounts do not accrue interest, as they are for transaction liquidity, not savings.

Required Documents for Opening:

Common Types:

AS ON DATE WE HAVE ONLY REGULAR CURRENT ACCOUNT

SAVINGS ACCOUNT

A savings account is a secure, interest-earning bank account designed for storing money, offering easy access for daily expenses while allowing balances to grow. These accounts typically provide

Key Considerations

How to Open a Savings Account

Required Documents: PAN card, Aadhaar card, proof of address, and passport-size photographs.

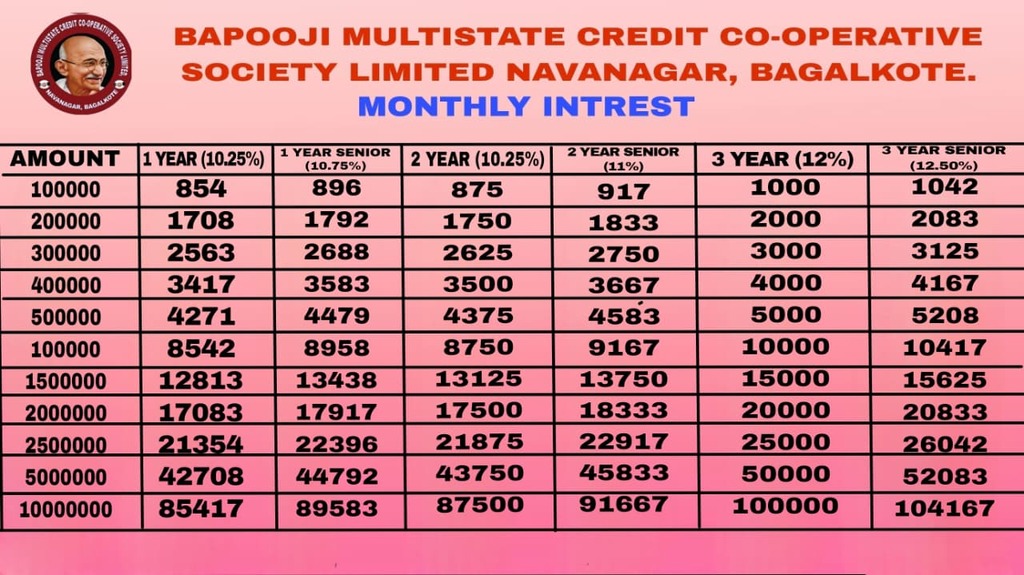

FIXED DEPOSIT

A Fixed Deposit (FD) is a low-risk, term investment offered by our society allowing you to lock in a lump sum for 30 days to 6 year 6 months at a guaranteed interest rate. Offering higher returns than savings accounts, FDs feature flexible payouts (monthly to annually) and provide higher interest rates for senior citizens, typically 0.50% more.

Key Features of Fixed Deposits

How to Open a Fixed Deposit

FDs can be opened at Head Office or at our society branches.

Documents Needed: PAN Card and KYC documents (Aadhaar, PAN)

Eligibility: Individuals, senior citizens, and non-individuals.

Common Uses

Disclaimer: premature withdrawal is usually subject to a penalty fee.

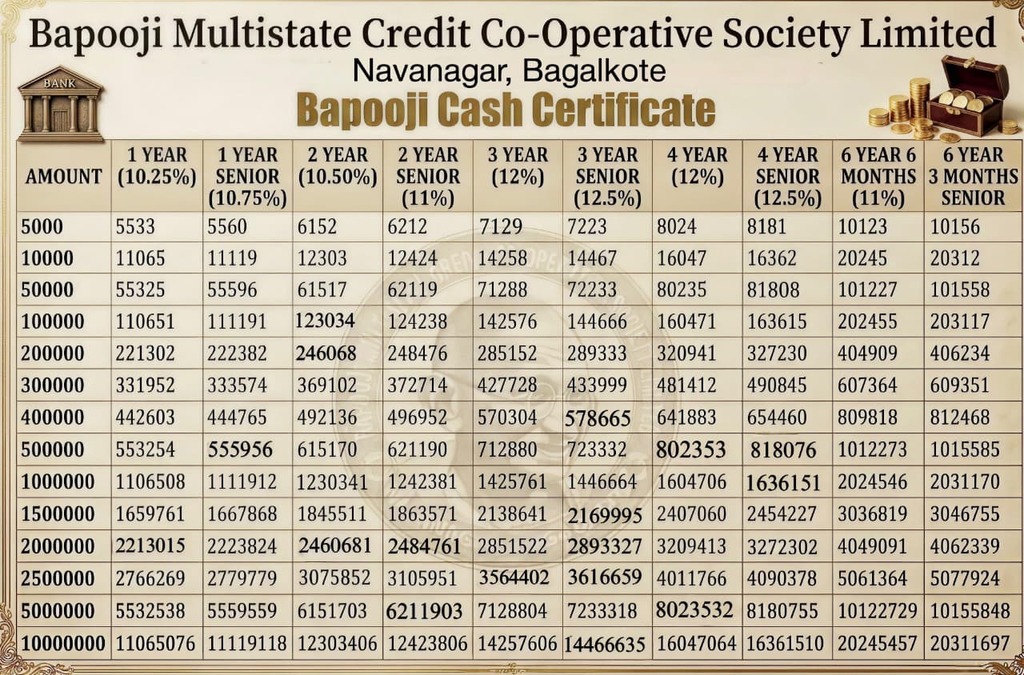

BAPOOJI CASH CERTIFICATE

A cumulative Fixed Deposit (BCC) is a type of investment where interest is compounded annually or quarterly and added back to the principal, paying out the total amount (principal + interest) only at maturity. It is ideal for long-term savings, offering higher returns compared to non-cumulative options due to the effect of compounding.

Key Features :

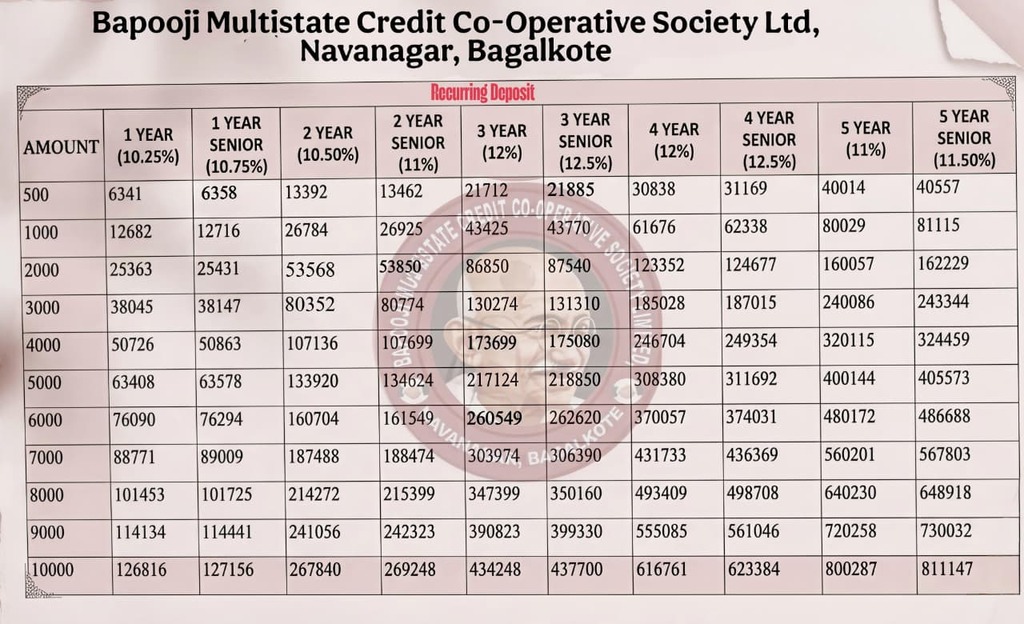

RECURRING DEPOSIT

A Recurring Deposit (RD) is a specialized term deposit offered by our society that allows individuals to deposit a fixed sum of money monthly for a specific tenure, earning a fixed interest rate (usually compounded quarterly). It is a safe, disciplined savings tool intended for building a corpus over time.

Key Features of Recurring Deposits:

Benefits:

TERM DEPOSIT

Coming Soon!!!!

Copyright © 2023 Bapooji Multistate Credit Co-Operative Society Limited, Navanagar , Bagalkote. All rights reserved.